Introduction

Auto insurance is one of those unavoidable expenses—necessary for legal driving, but often confusing and frustrating when it comes to finding the best price. In 2025, the hunt for cheap auto insurance is more competitive (and more complex) than ever. With rising inflation, evolving driving habits, and tech-savvy insurers introducing new pricing models, today’s consumers must be smarter than ever before.

The good news? There are real, practical ways to significantly reduce your premiums without compromising on coverage. Whether you’re a student, a family driver, or someone just looking to trim the fat from your monthly bills, this comprehensive guide is your roadmap to navigating the world of budget-friendly auto insurance.

We’ll break down exactly how insurers price policies, expose common pricing traps, and reveal how you can use emerging trends to your advantage. From choosing the right company to unlocking discounts you never knew existed, you’ll walk away from this guide fully equipped to make confident, cost-effective decisions.

Ready to unlock serious savings? Let’s get started.

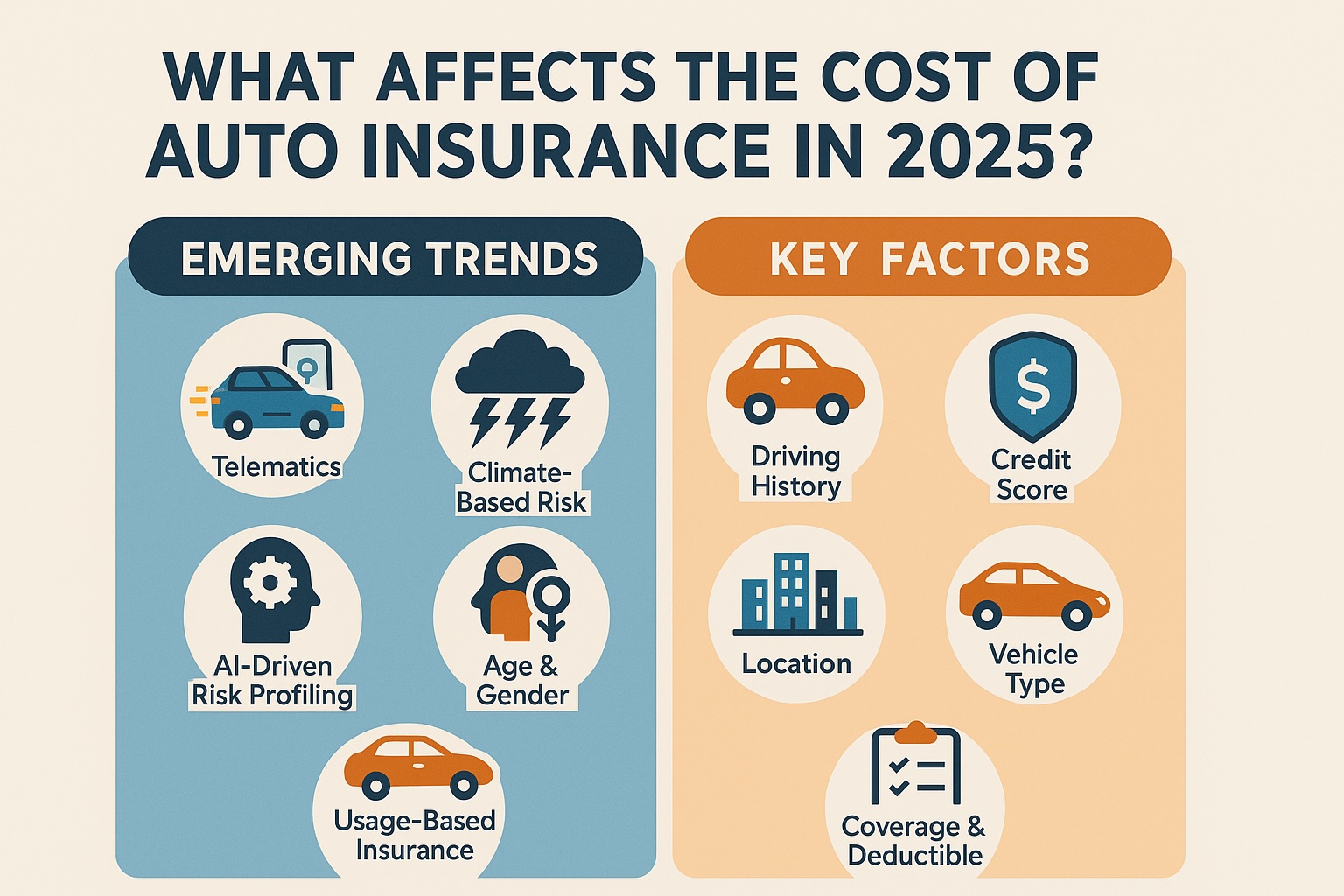

What Affects the Cost of Auto Insurance in 2025?

Finding cheap auto insurance starts with understanding the moving parts that go into pricing. Insurers don’t just pull numbers out of a hat—they rely on a complex formula that evaluates risk, location, lifestyle, and even market trends. In 2025, these factors are shifting thanks to technology, climate change, and a more competitive insurance market.

Emerging Trends in Insurance Pricing

Technology is reshaping how premiums are calculated. In 2025, many insurers use telematics—real-time driving data collected via apps or in-vehicle devices. Your speed, braking habits, time of day you drive, and even your phone usage behind the wheel are tracked and used to offer you lower (or higher) rates.

Another trend is climate-based risk adjustments. With an increase in natural disasters like wildfires, floods, and hailstorms, insurers are factoring regional climate risks into your premiums. That means living in a high-risk zone—even if you’ve never filed a claim—can affect your cost.

AI-driven risk profiling is also becoming mainstream. Using machine learning algorithms, insurers assess millions of data points to fine-tune your personal risk score. This can lead to hyper-personalized pricing—but it also means your quote could vary wildly between providers.

Lastly, the rise of usage-based and pay-per-mile insurance is a game-changer for low-mileage drivers. If you work from home or drive only occasionally, this could drastically reduce your monthly premiums.

Key Factors Insurers Consider When Calculating Rates

Despite new trends, traditional factors still play a major role in determining your premium:

-

Driving history: Accidents, speeding tickets, and DUIs raise your rates.

-

Age and gender: Young drivers, especially males under 25, often pay more.

-

Credit score: Yes, in most states, poor credit can mean higher premiums.

-

Location: Urban areas with high accident or theft rates usually cost more.

-

Vehicle type: Sports cars or luxury vehicles are more expensive to insure.

-

Coverage level and deductible: Choosing a higher deductible lowers your premium, but increases out-of-pocket costs in the event of a claim.

Insurers also consider how long you’ve been continuously insured, whether you own or lease your car, and even your occupation in some cases. The more they know about your habits and history, the more precisely they can price your policy.

Top Strategies to Score Cheap Auto Insurance

Now that you know what influences your rates, it’s time to flip the script and focus on how to reduce them. Getting cheap auto insurance in 2025 is about working smarter, not sacrificing essential protection. It’s not just about picking the lowest number—it’s about finding maximum value for your dollar.

Comparison Shopping Like a Pro

One of the simplest yet most powerful tools at your disposal is comparison shopping. Rates can vary dramatically from one insurer to another—even for the exact same driver profile. That’s why it’s crucial to get quotes from at least 3–5 providers before committing.

When comparing, make sure you’re looking at identical coverage levels and deductibles. Some quotes appear cheaper but offer less protection. Use reliable comparison tools like:

-

The Zebra

-

NerdWallet

-

Policygenius

-

Gabi

These platforms often use soft credit checks, which won’t impact your score. And don’t just check once—review your options annually. Rates change based on market shifts, your updated profile, and insurer-specific pricing models.

Also, inquire about local or regional insurers. They might not have national name recognition, but many offer competitive rates and better customer service tailored to your area.

Leveraging Discounts and Bundling Options

The discount game is where many people leave money on the table. Nearly every insurer offers dozens of potential discounts, including:

-

Safe driver programs

-

Low mileage or telematics-based incentives

-

Good student (for drivers under 25)

-

Military/veteran status

-

Anti-theft devices or vehicle safety features

-

Paperless billing or autopay enrollment

In 2025, many providers now offer smartphone app tracking for discounts through usage-based insurance. If you’re a cautious driver, this could shave off 10–30% of your bill.

Then there’s bundling. Combining your auto insurance with homeowners, renters, or even life insurance can unlock substantial discounts—often up to 25%. But don’t assume bundling always means cheaper. Do the math to verify that the combined rate is genuinely less than buying policies separately.

Lastly, ask about unadvertised discounts. Some are available but not listed online. A simple question to your agent like, “Are there any additional discounts I may qualify for?” could make a surprising difference.

Best Cheap Auto Insurance Providers in 2025

When you’re on the hunt for cheap auto insurance, knowing where to look is half the battle. Not all insurance companies are created equal—some specialize in low-cost coverage, while others offer rock-solid service with competitive rates. In 2025, a mix of legacy providers and tech-driven newcomers are dominating the affordability space.

Companies Offering Competitive Rates

Here are some of the top providers known for offering cheap auto insurance in 2025:

-

GEICO: Still a leader for affordability and ease of use. Their online tools make customizing and adjusting policies simple, especially for younger drivers.

-

Progressive: Ideal for high-risk drivers or those with imperfect records. Their Name Your Price tool helps tailor coverage within your budget.

-

State Farm: Offers solid rates for drivers with clean records and great bundling options if you own a home or multiple cars.

-

Nationwide: Known for usage-based insurance (SmartRide), which rewards good driving habits with steep discounts.

-

Liberty Mutual: Offers customizable coverage, great multi-policy discounts, and competitive pricing for families and safe drivers.

-

Root Insurance & Metromile: These newer, app-based insurers use telematics and pay-per-mile pricing to cater to occasional drivers and remote workers.

Every provider prices differently based on your location, age, driving record, and vehicle. That’s why it’s critical to compare personalized quotes, not just reviews.

Reviews & Reliability: What to Look For

It’s tempting to jump on the lowest rate, but don’t overlook service quality. Consider the following before committing:

-

Claim satisfaction: Cheap doesn’t mean much if your claim is denied or delayed. Look for high ratings from J.D. Power or NAIC complaint indexes.

-

Customer support: Does the company offer 24/7 support, local agents, or chat-based assistance? These extras are invaluable during stressful times.

-

Mobile tools: Can you file claims, adjust coverage, and view documents on an app? In 2025, digital ease matters more than ever.

-

Financial stability: Check AM Best or Moody’s ratings. You want a company that can actually pay out claims when it counts.

Also, explore insurance reviews and forums on sites like Reddit’s r/Insurance or Trustpilot. These can offer unfiltered insights into how a company treats its policyholders during disputes and claims.

Ultimately, the best cheap auto insurance provider is the one that balances low costs with dependable service, easy policy management, and relevant coverage options.

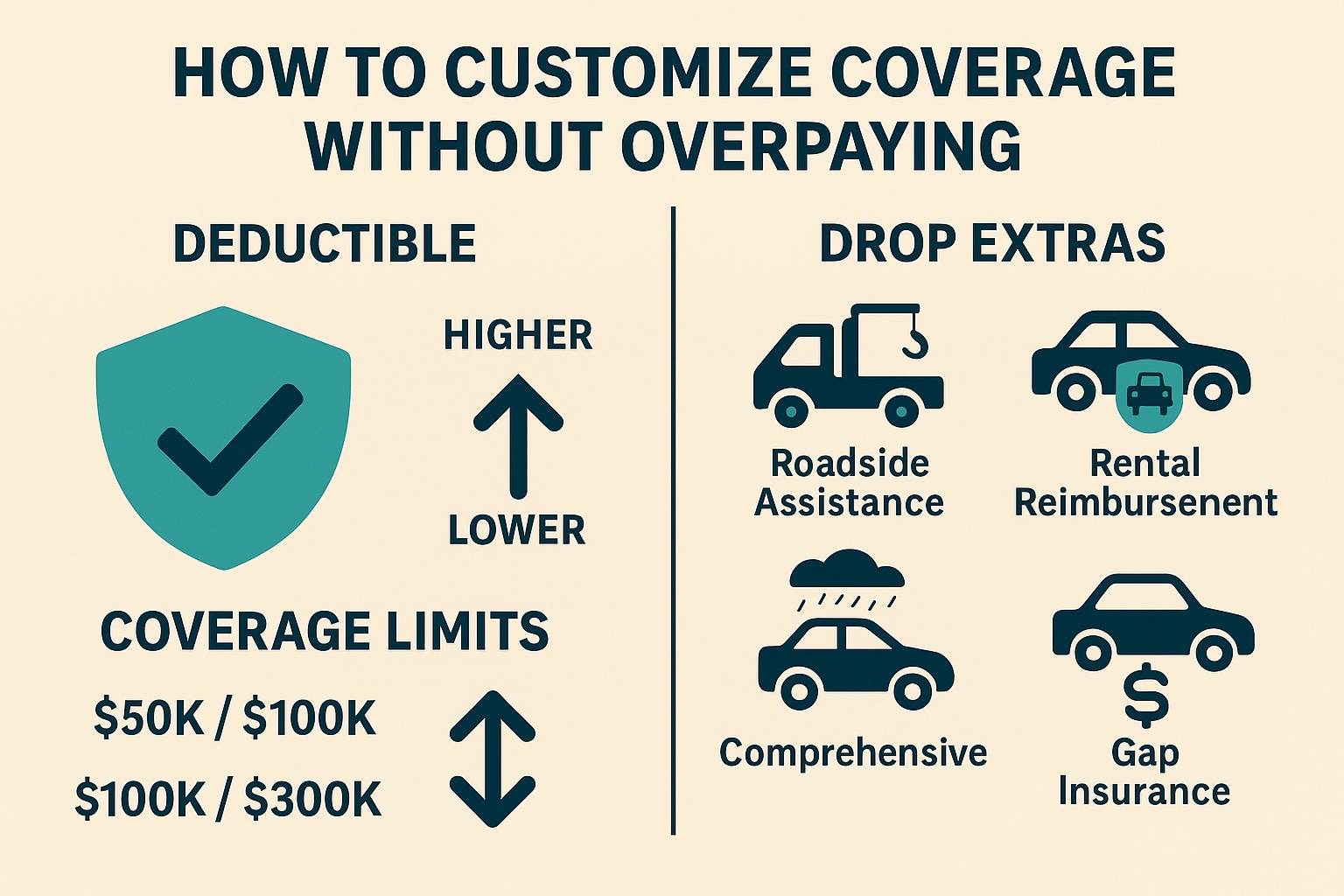

How to Customize Coverage Without Overpaying

One of the best ways to unlock cheap auto insurance in 2025 is to tailor your policy to match your actual needs. Too often, people overpay for coverage they don’t use—or worse, under-insure themselves in critical areas. With a little knowledge and fine-tuning, you can build a policy that offers solid protection at a surprisingly low cost.

Choosing the Right Deductible and Limits

Deductibles and coverage limits are the two levers that most directly affect your premium:

-

Higher deductibles = lower premiums: Opting for a $1,000 deductible instead of $250 could save you hundreds annually. Just make sure you can afford that amount out of pocket in the event of a claim.

-

Lower limits = riskier exposure: Don’t skimp too much on liability coverage. State minimums often fall short in real-world accidents. Aim for at least $100,000/$300,000 for bodily injury and $100,000 for property damage if you have any assets to protect.

Strike a balance based on your driving habits, car value, financial cushion, and risk tolerance. For example, a newer driver with an older vehicle might choose high deductibles and minimal comprehensive coverage to cut costs.

Dropping Extras You Don’t Actually Need

Many policies come loaded with optional coverages that may not be necessary for everyone. Here’s where you can potentially save big:

-

Roadside assistance: If you already have AAA or a credit card that includes this, you don’t need to pay for it twice.

-

Rental reimbursement: Not needed if you have a backup vehicle or access to alternative transport.

-

Comprehensive coverage: Consider dropping this if your car is worth less than a few thousand dollars—especially if the deductible would exceed a significant portion of its value.

-

Gap insurance: Only essential if your car loan or lease balance exceeds your car’s current market value.

Additionally, review your usage. If you drive under 7,500 miles a year, you might qualify for low-mileage discounts or benefit more from pay-per-mile insurance.

Don’t forget to ask your agent to walk through your declarations page line by line. Sometimes removing or adjusting one small line item can lead to a surprising premium drop.

Mistakes That Make Your Insurance More Expensive

Even when you’re doing everything right to find cheap auto insurance, a few common missteps can sabotage your efforts. These mistakes can quietly inflate your premiums—or worse, cause you to lose valuable coverage. Here’s what to avoid if you’re serious about cutting costs in 2025.

Overlooking Usage-Based Insurance Programs

One of the biggest missed opportunities in 2025 is not enrolling in usage-based insurance (UBI) or telematics programs. These programs reward drivers for safe habits like gentle braking, low-speed driving, and not using a phone behind the wheel. All you need is a smartphone or a plug-in device.

Many drivers avoid these programs due to privacy concerns, but the savings can be substantial—up to 30% or more in some cases. If you rarely drive or stick to daytime, local trips, UBI can significantly lower your rates.

Tip: Ask your provider if they offer “try-before-you-buy” apps that monitor your driving for a few weeks without commitment. You’ll get an estimated discount upfront.

The Loyalty Trap and How to Escape It

Sticking with the same insurer year after year might seem like a good move, but it often leads to paying more than necessary. Many companies engage in price optimization—raising premiums gradually because they believe loyal customers are less likely to switch.

Escaping this trap requires you to:

-

Compare quotes every year, even if you’re happy with your current provider.

-

Ask your insurer for a re-rate, especially after life events like moving, getting married, or improving your credit score.

-

Mention competitor quotes during renewal. Insurers often have price-match flexibility.

-

Look for first-time customer deals and cash-back offers when switching providers.

Other subtle mistakes include:

-

Paying monthly instead of annually (monthly plans often include extra processing fees).

-

Failing to update mileage when you drive less due to lifestyle changes.

-

Not removing ex-drivers (like adult kids) who no longer use the car.

Avoiding these common pitfalls helps you make the most of the savings opportunities that already exist—no tricks, no gimmicks, just smart strategy.