Introduction

Car insurance is one of those necessary evils in life something you’re legally required to have, but often left confused by what it really offers. On the surface, it seems like just another bill. Dig a little deeper, though, and you’ll uncover a complex world of hidden fees, misunderstood policies, and surprising truths that could cost you big time or save you thousands. Whether you’re a new driver, a seasoned motorist, or just looking to renew your policy, understanding the fine print of your coverage can make all the difference.

This article uncovers seven brutally honest truths about car insurance truths that your provider likely doesn’t want you to know. From how insurers really calculate your premiums to why staying loyal can actually hurt your wallet, we’re going beyond the marketing fluff. By the time you’re done reading, you’ll not only be smarter about your policy you might even be ready to challenge it.

Ready to stop overpaying and start understanding? Let’s get into it.

The Reality Behind Car Insurance Premiums

Understanding how your car insurance premium is calculated is a bit like pulling back the curtain on a magic show—suddenly, what felt arbitrary starts to make (somewhat infuriating) sense. Insurers don’t just roll a dice to decide your rate. Instead, they rely on a set of detailed factors that statistically determine how “risky” you are as a customer.

How Your Profile Impacts Premium Rates

First and foremost, your personal profile is a major factor. This includes your age, gender, marital status, and even your occupation. For example, young male drivers under 25 typically pay higher rates because statistically, they’re more likely to be involved in accidents. Likewise, someone working as a delivery driver may pay more than an accountant who drives once a day.

But it doesn’t stop there. Driving history also plays a massive role. If you’ve had past claims, traffic violations, or accidents, even if they weren’t your fault, your rate climbs. Insurers use this data to build a risk profile that helps them predict future behaviors. In essence, the cleaner your driving record, the better your rate.

On top of this, insurance history is factored in. If you’ve had lapses in coverage, switched providers too often, or made several claims in a short time, you’re labeled high-risk. That label comes with a price tag.

The Role of Location, Vehicle Type & Driving History

Where you live might have more to do with your premium than you think. Insurance companies track regional statistics everything from accident rates, theft reports, population density, and weather risks. So even if you’ve never had a fender bender, living in a high-crime area or a flood-prone zone can inflate your premium.

Your car’s make and model also matter. A high-performance vehicle or a luxury model usually costs more to insure than a modest sedan, not just because of repair costs, but because they’re often involved in more claims. Additionally, the frequency with which your model is stolen also affects rates—some cars are theft magnets, and insurers adjust accordingly.

And let’s not forget annual mileage. The more you drive, the higher your chances of being involved in an incident. People who clock in over 15,000 miles a year are statistically more likely to file a claim than someone who drives only on weekends.

What Car Insurance Actually Covers (and What It Doesn’t)

When you purchase car insurance, you’re handed a stack of paperwork filled with legalese and fine print that’s easy to skim and hard to understand. Many people assume that if they’re insured, they’re completely protected from any mishap. Unfortunately, that’s far from the truth. The coverage you think you have and what you actually have are often two very different things.

Common Misconceptions About Coverage

One of the biggest misunderstandings about car insurance is the idea that it covers any and all types of damage. In reality, most policies are broken down into specific types of coverage, each handling different situations. For instance:

-

Liability insurance covers damages you cause to other people or property, but not your own car.

-

Collision insurance covers damage to your car in an accident regardless of who’s at fault.

-

Comprehensive insurance handles non-collision-related incidents like theft, fire, vandalism, or weather damage.

What’s more, some drivers assume their insurance will automatically cover rental cars, roadside assistance, or medical payments. In many cases, those require separate add-ons or endorsements.

Also, if you’re using your vehicle for business purposes like food delivery or ride-sharing your personal policy likely won’t cover any incidents that occur during those activities. You’d need a commercial auto policy or specific endorsements for that.

The Fine Print: Exclusions and Limitations

Every insurance policy contains exclusions situations or items not covered no matter what. These can be buried deep in the documentation and easy to overlook. For example, most policies won’t cover mechanical failures or regular wear and tear. So if your engine dies or your transmission gives out, don’t expect your insurer to foot the bill.

Then there are coverage limits. Each portion of your policy has a financial cap go over it, and you’re paying the rest out of pocket. Let’s say your liability limit is $50,000 and you cause an accident that results in $100,000 in damages you’re on the hook for the other $50,000.

Another kicker? Depreciation. Many insurers only pay out the “actual cash value” of your vehicle, not the price you paid for it. That means if your brand-new car is totaled a year after purchase, the payout could be thousands less than you expect.

In short, the fine print matters. If you haven’t read your policy front to back, you might be relying on coverage that doesn’t actually exist. Knowing what’s covered and more importantly, what’s not can save you from devastating financial surprises down the road.

The Truth About Minimum Coverage Requirements

Most states have laws mandating a minimum level of car insurance. It’s tempting to assume that meeting these minimums means you’re fully protected but this couldn’t be further from the truth. In reality, state minimums often provide only a basic safety net, leaving you vulnerable to massive out-of-pocket costs if disaster strikes.

Why Minimum Isn’t Always Enough

Minimum coverage is designed to protect other people, not necessarily you. In nearly every case, it includes bodily injury and property damage liability meaning if you cause an accident, your insurance will pay for the other party’s medical expenses or car repairs up to a limited amount. That’s it.

Let’s say your state requires $25,000 in bodily injury coverage. Sounds decent, right? But consider this: one trip to the ER with surgery and follow-up care can easily exceed that. If you’re at fault, and the total cost is $100,000, you’ll be responsible for the remaining $75,000 potentially putting your savings, assets, or even home at risk.

Minimum coverage also typically doesn’t include collision or comprehensive insurance. That means damage to your own car in an accident, theft, natural disasters, or vandalism isn’t covered unless you add those extras to your policy. Many drivers find out too late that they’re on the hook for repairs or replacement out of pocket.

How to Determine the Right Coverage Level

So, how much coverage do you actually need? The answer depends on your financial situation, risk tolerance, and driving habits.

If you drive an expensive vehicle, live in a high-traffic area, or park on the street, you may want to opt for comprehensive and collision coverage to protect your own investment. If you have significant savings or assets, you’ll also want to increase your liability limits to guard against lawsuits and high medical bills.

Experts often recommend liability limits of at least $100,000/$300,000 for bodily injury and $100,000 for property damage. It might cost a bit more in premiums, but it’s a small price to pay compared to the financial fallout of inadequate coverage.

You should also consider uninsured/underinsured motorist protection, which covers you if the other driver has no insurance or not enough. This is especially important in areas where many drivers go uninsured.

Lastly, speak with a licensed insurance advisor to do a full risk assessment. They can help tailor a policy that fits your specific needs, avoiding both underinsurance and unnecessary expenses.

How Insurers REALLY Handle Claims

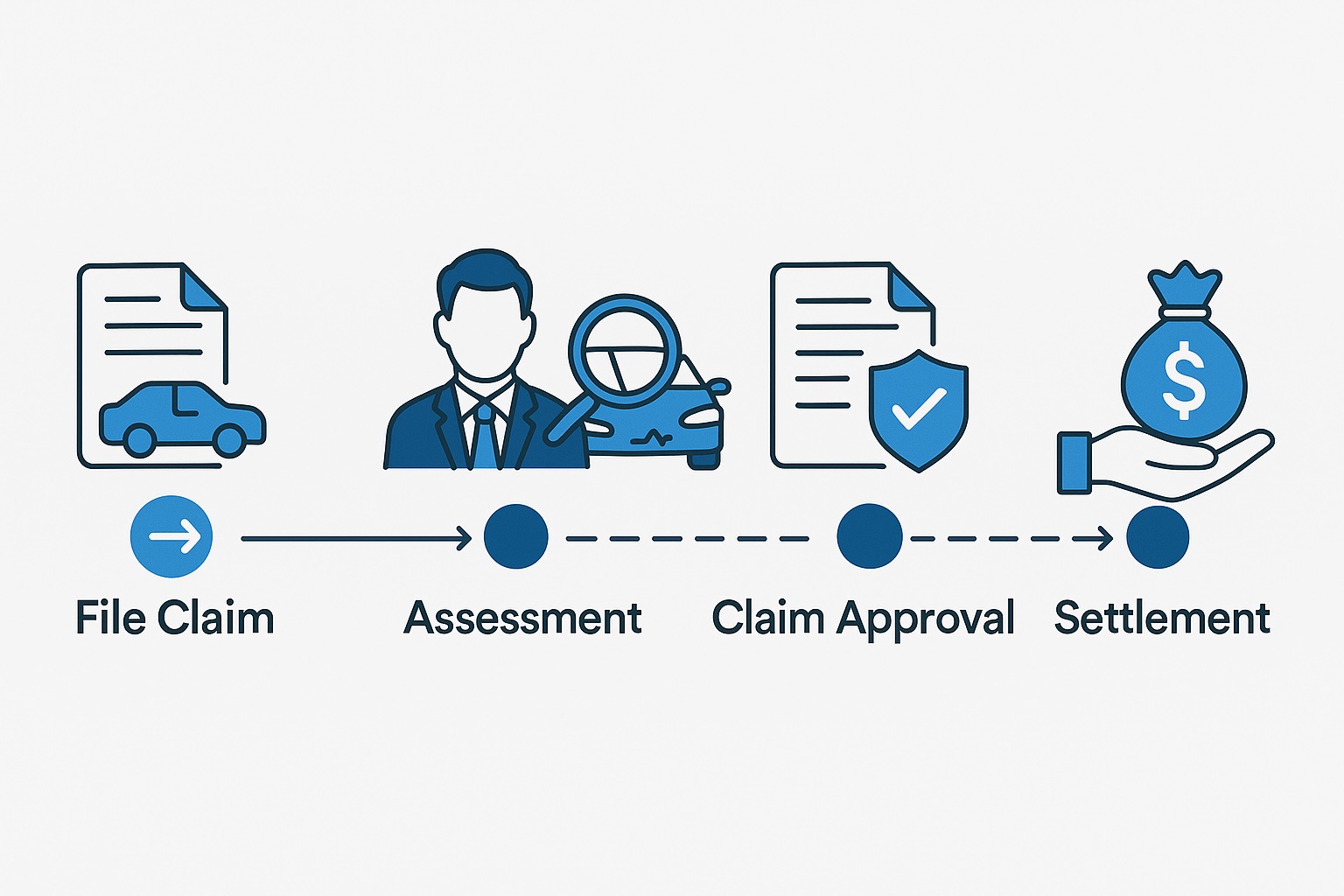

Filing a car insurance claim can feel like launching a paper airplane into a tornado—uncertain, slow, and often more frustrating than you imagined. Insurers often promise a smooth, hassle-free process, but behind the scenes, there’s a rigorous system in place that prioritizes cost control over customer satisfaction. Understanding how claims are truly handled will prepare you for what lies ahead when the unexpected strikes.

The Claim Approval Process Demystified

The process typically starts when you report an incident usually via a mobile app, website, or a phone call. From there, your case is assigned to a claims adjuster, who is responsible for investigating the details. Their job is to assess the damage, determine who’s at fault, and decide how much (if anything) the insurer should pay.

Contrary to popular belief, the adjuster works for the insurance company not for you. Their goal is to limit payouts while maintaining policy compliance. So, while they may seem friendly and helpful, their priority is protecting the company’s bottom line.

They’ll look at the police report, photos of the damage, medical bills, and may even interview witnesses. They might send you to a preferred repair shop, which can mean lower costs for the insurer but not necessarily better results for you. If the claim involves injuries, they’ll request medical records and may question the necessity or timing of your treatments.

In many cases, they’ll offer a settlement amount quickly a tactic to minimize the chance of you disputing the figure or hiring a lawyer. Unfortunately, many policyholders accept these early offers without realizing they could be entitled to more.

What Can Delay or Deny Your Claim

Several factors can drag your claim through the mud—or get it flat-out denied. Here’s what you should watch out for:

-

Incomplete or inconsistent documentation: Missing police reports, blurry photos, or conflicting statements can cause delays.

-

Late reporting: Most policies require prompt notification of any incident. Waiting too long can be grounds for denial.

-

Pre-existing damage: If they believe the damage wasn’t caused by the current incident, they’ll reject it.

-

Policy exclusions: If the claim involves a situation your policy doesn’t cover like using your car for rideshare without a proper endorsement it’s an automatic denial.

-

Disputed liability: If fault isn’t clear or there’s conflicting testimony, the process can stall while both parties fight it out.

To protect yourself, always document everything immediately after an incident. Take photos from every angle, collect witness info, and keep receipts for any out-of-pocket expenses. If your claim is denied or undervalued, you have the right to appeal or file a complaint with your state’s insurance department.

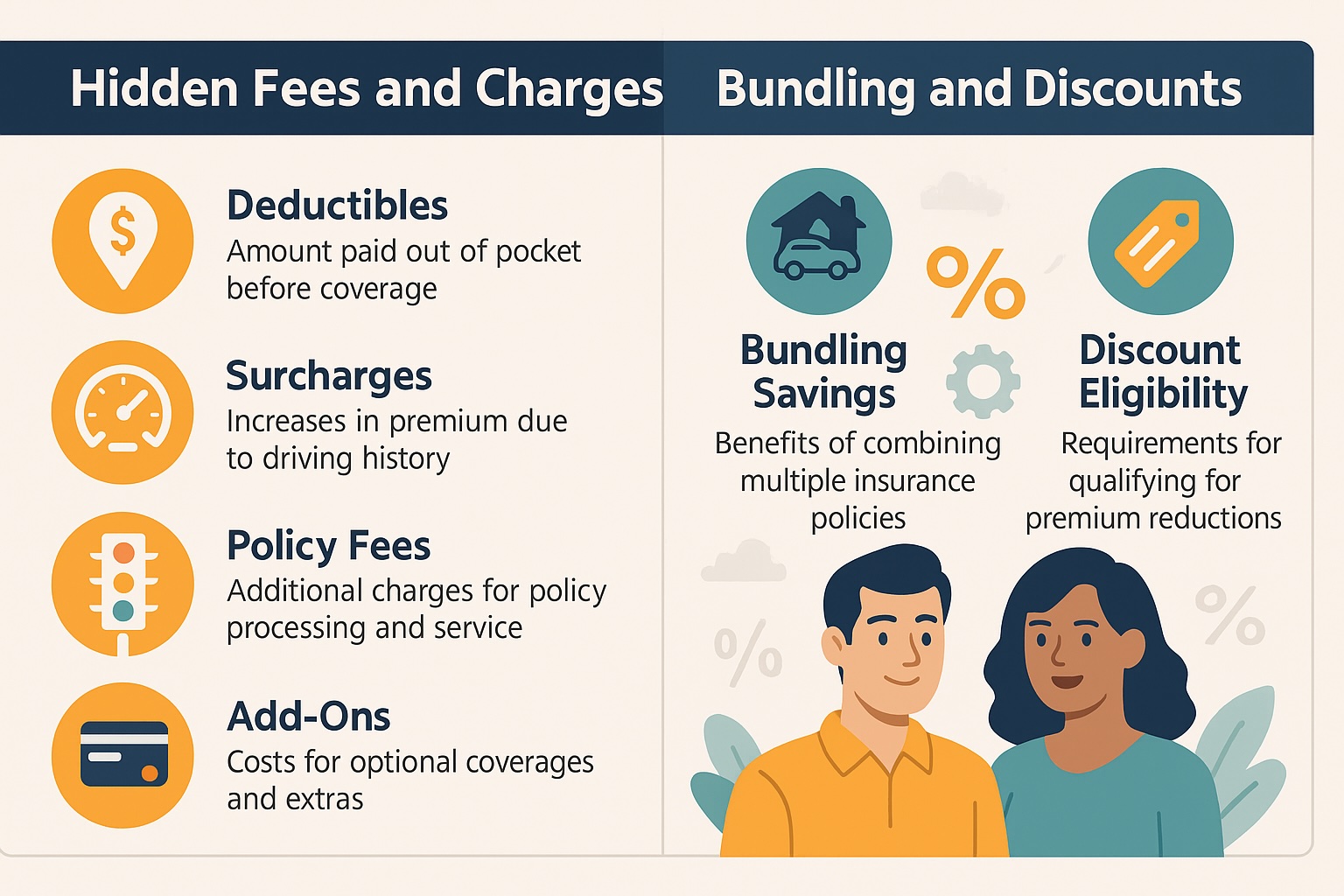

Hidden Fees and Surprising Charges

Think your monthly premium is the only cost tied to your car insurance? Think again. Insurance policies often come with a host of hidden fees, surcharges, and optional add-ons that can quietly drain your wallet. Understanding these lesser-known charges can help you avoid unpleasant surprises and possibly negotiate a better deal.

Understanding Deductibles and Surcharges

One of the most misunderstood elements in a car insurance policy is the deductible the amount you pay out of pocket before your coverage kicks in. While a higher deductible usually means a lower premium, it also means you’ll be stuck with a bigger bill if an accident occurs. For instance, if you set a $1,000 deductible and file a claim for $1,200 in damage, the insurer only pays $200.

Then there are surcharges, which are added to your premium due to specific “risk-enhancing” events. These can include:

-

Traffic violations (even minor ones like rolling through a stop sign)

-

At-fault accidents

-

Lapses in coverage

-

Filing multiple claims within a short period

These charges can stay on your record for up to three years, and in some cases, they’re applied automatically even if the claim wasn’t your fault.

How Bundling and Discounts Actually Work

Insurance companies love to advertise bundling discounts: combine your car, home, and sometimes even life insurance, and you’ll save big. While this can offer savings, the actual discount may be less than you think. Sometimes, individual policies from separate providers can cost less than a bundled package especially if the bundled provider is inflating your base rate before applying the discount.

Other common discounts include:

-

Safe driver discount

-

Good student discount

-

Low mileage discount

-

Anti-theft device discount

But here’s the kicker: discounts are often based on fine print and very specific eligibility rules. Miss one document or cross a mileage threshold, and the discount disappears.

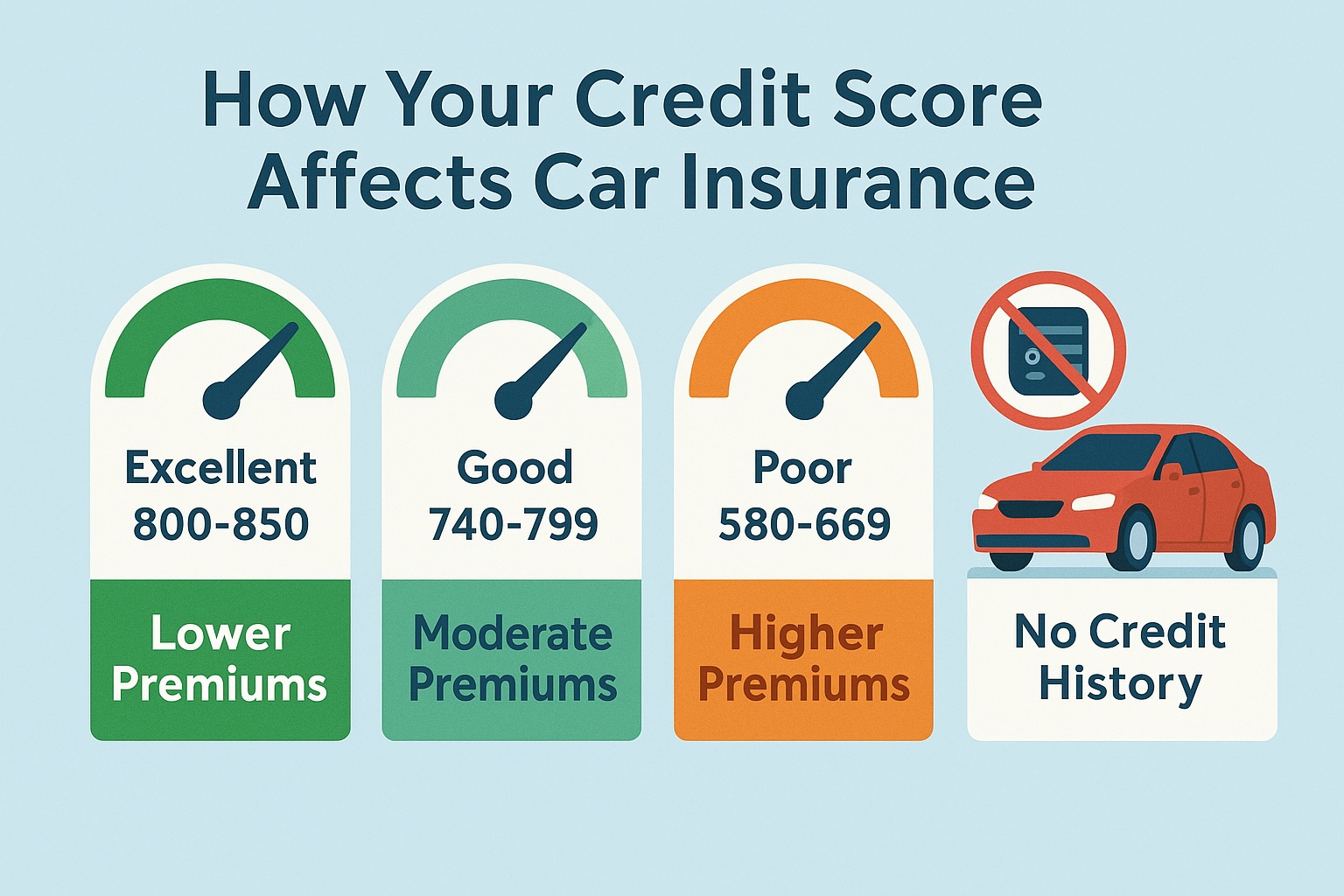

How Your Credit Score Affects Car Insurance

You might think your credit score only matters when buying a house or applying for a credit card but insurance companies beg to differ. In most states, your credit-based insurance score is one of the strongest predictors of your premium. It’s a controversial practice, and many drivers are shocked to learn just how much their score influences their rate.

Why Insurers Use Credit-Based Scores

Insurance providers argue that people with higher credit scores are statistically less likely to file claims. They use what’s known as a credit-based insurance score a variant of your traditional credit score to assess risk. This score is built using factors like:

-

Length of credit history

-

Outstanding debt

-

Payment history

-

Credit utilization ratio

-

Number of credit inquiries

Notably, this score doesn’t include your income or employment status, and insurers claim it’s purely based on risk analytics.

States like California, Hawaii, and Massachusetts have banned the use of credit scores in car insurance calculations. But in most other states, insurers are legally allowed to use this data and they do so aggressively.

If your score drops due to missed payments, rising debt, or even identity theft, you could see your premium spike even if your driving record remains spotless. On the flip side, improving your score can help lower your rates over time.

Tips to Improve Your Rate Without Changing Plans

Fortunately, there are ways to improve your credit profile and possibly reduce your insurance costs—without switching insurers:

-

Pay all bills on time – This has the largest impact on your credit score.

-

Reduce outstanding debt – Lowering your credit card balances improves your utilization ratio.

-

Avoid hard inquiries – Too many credit checks in a short time can ding your score.

-

Keep old accounts open – A long credit history boosts your reliability score.

-

Dispute any errors – Check your credit reports from Equifax, Experian, and TransUnion for inaccuracies.

In addition to credit management, ask your insurer to re-evaluate your policy every 6–12 months. If your credit score improves, you might qualify for a better rate.

Also, check if your insurer uses a “soft pull” (which doesn’t affect your score) or a “hard pull” (which can slightly reduce it) when assessing your credit. Most do soft pulls, but it’s always good to verify.

Being proactive about your credit and understanding how it affects your insurance could make a bigger difference than you think.

The Loyalty Trap: When Sticking With One Insurer Hurts You

Loyalty should be rewarded, right? Unfortunately, when it comes to car insurance, staying with the same provider year after year can actually end up costing you more. This is known in the industry as “price optimization” a practice where insurers raise your rates based on your predicted loyalty, not because of increased risk.

Why Long-Term Customers May Pay More

Insurers track your behavior over time, and if you’ve remained with them for years without switching or shopping around, they may classify you as a “low-risk switcher.” In other words, they believe you’re unlikely to leave even if your premium increases. As a result, your renewal rates might rise incrementally each year, even if you haven’t filed a claim or changed your driving habits.

This practice isn’t universal, but it’s common enough that regulators in some states have banned or restricted it. Still, millions of drivers are paying the so-called “loyalty tax” without even realizing it.

Furthermore, insurers may phase out discounts over time such as safe driving bonuses or multi-car savings unless you call and renegotiate. And if you haven’t updated your driving profile (mileage, commute, garage location), you could be missing out on significant savings.

In contrast, new customers often receive aggressive introductory rates, especially if they’re switching from a major competitor. It’s ironic but true shopping for a new policy every year or two can keep your premiums lower than remaining loyal.

Smart Strategies for Switching Providers

If you suspect you’re overpaying, here’s how to exit the loyalty trap smartly:

-

Compare quotes annually from at least 3–5 insurers.

-

Use insurance comparison tools that allow soft credit pulls to prevent score dings.

-

Look for bundling or switcher bonuses that can reduce your total costs.

-

Time your switch a few weeks before renewal to avoid lapses or penalties.

-

Ask your current insurer to match or beat competitor offers they often will.

-

Ensure your new policy overlaps the old one by at least a day to avoid coverage gaps.

Also, don’t cancel a policy before your new one is active. A lapse in coverage even for a day can increase your future premiums or make you ineligible for certain discounts.

Insurance companies rely on inertia. By actively managing your policy, asking questions, and not being afraid to switch, you can escape the loyalty trap and find the best value for your money.

Conclusion

Understanding car insurance isn’t just about fulfilling a legal requirement it’s about protecting your finances, your vehicle, and your peace of mind. From uncovering how premiums are calculated to revealing the shocking truth about loyalty penalties, you’ve now got a 360-degree view of what really goes on behind the scenes.

The key takeaway? Never take your car insurance policy at face value. Every clause, every rate hike, every discount or lack thereof has a reason behind it. Knowing these seven brutally honest truths empowers you to take control, ask sharper questions, compare providers, and make smarter financial decisions.

So, whether you’re shopping for a new policy or reconsidering your current one, don’t settle for surface-level promises. Use this knowledge to ensure you’re not just insured but smartly insured.

Frequently Asked Questions

Is it bad to only carry minimum car insurance coverage?

Yes, in many cases. While it meets legal requirements, it often leaves you financially exposed in major accidents or theft scenarios.

How often should I shop around for car insurance?

Ideally, once a year. Rates change, and staying loyal without comparison can cost you hundreds annually.

Does my credit score really affect my premium that much?

In most states, yes. A poor credit score can lead to significantly higher premiums—even with a perfect driving record.

What should I do if my car insurance claim is denied?

Start by reviewing the denial reason, gather supporting documentation, and request a formal review. If needed, contact your state insurance regulator.

Are online insurance quote tools accurate?

They’re a good starting point, but not always fully accurate. Insurers may adjust quotes after pulling full records and credit data.

Can bundling policies really save me money?

Sometimes. But always compare bundled quotes with separate policies to ensure you’re actually saving money.